Why do consumers feel worse in a strong economy?

Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

Headline economic indicators remain resilient as gross domestic product (GDP) continues to expand, the unemployment rate remains low and wage growth has held up better than expected. However, these figures reflect averages, not the lived experience of households. A growing number of consumers continue to face pressure from elevated costs for essentials such as housing, food and healthcare. More recently, rising gasoline prices have added to this strain, particularly for lower- and middle-income households.

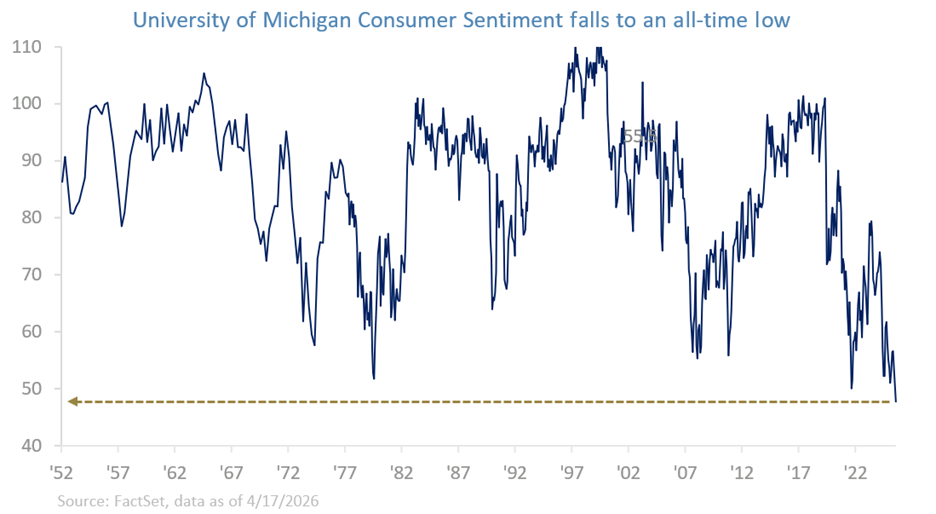

As a result, despite broadly solid economic data, consumer sentiment has remained subdued, highlighting the gap between aggregate performance and day-to-day financial reality. The good news this week was that, despite increasing to multi-month highs, both import prices and producer prices came in softer than expected, which should provide some support to investor sentiment by reinforcing the disinflation narrative. Looking ahead, next Friday’s final estimate of consumer sentiment will be in focus. We expect a modest improvement, reflecting some easing in geopolitical tensions in the Middle East, although sentiment is likely to remain depressed and near historically low levels.

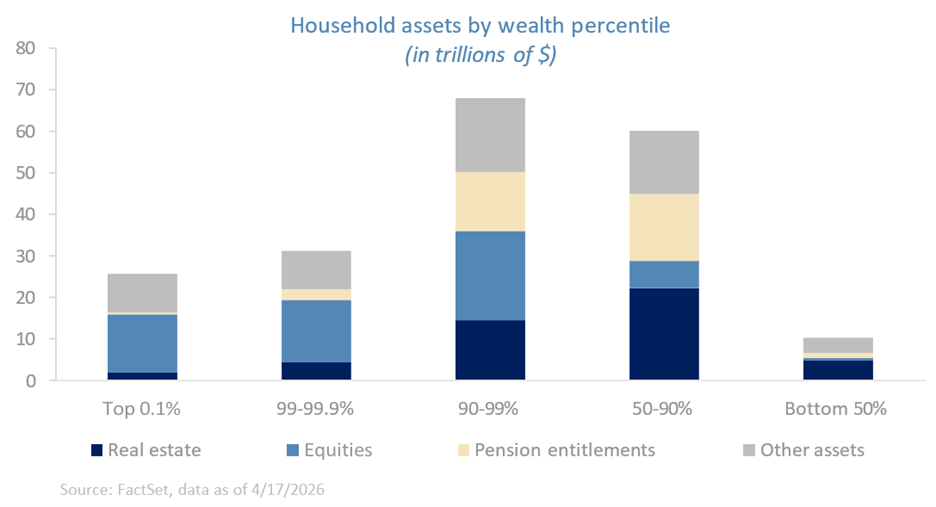

This is what has been described as a “K-shaped” economy, which describes an economic recovery in which outcomes diverge across income groups. Higher-income households have generally benefited from rising asset prices, including equities and home values, as well as more stable employment. In contrast, lower-and middle-income households tend to have less exposure to financial markets and are more likely to rent rather than own homes, limiting their participation in recent wealth gains. The sharp increase in home prices since the pandemic and elevated mortgage rates has made homeownership less accessible, further widening the gap between those building wealth and those primarily managing rising expenses.

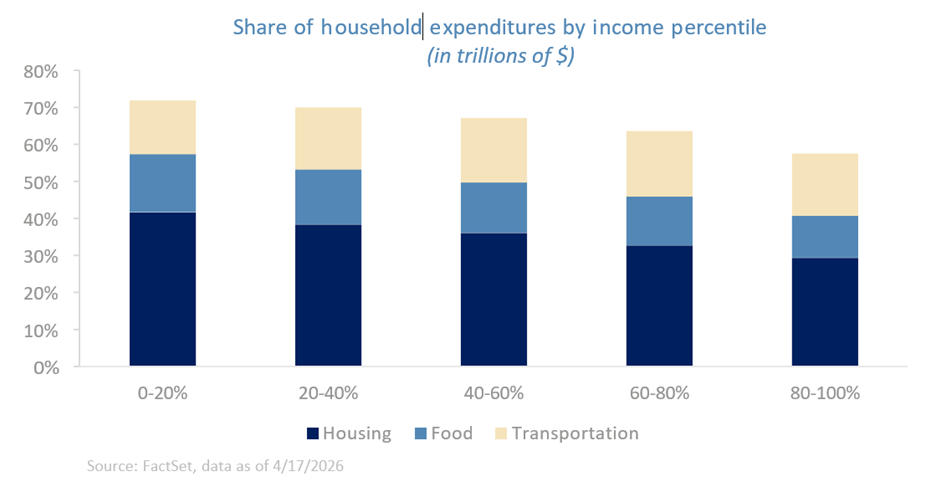

While inflation has moderated significantly from its peak in 2022, it remains above the Federal Reserve’s long-term target of 2%, and it impacts households differently. Lower-income households allocate a larger share of their income to non-discretionary expenses such as rent, food and energy, categories that have experienced persistent price pressures. Higher-income households, by contrast, tend to have greater financial flexibility and are less impacted these essential cost increases as a share of income. This dynamic reinforces the divergence in financial experiences across income groups.

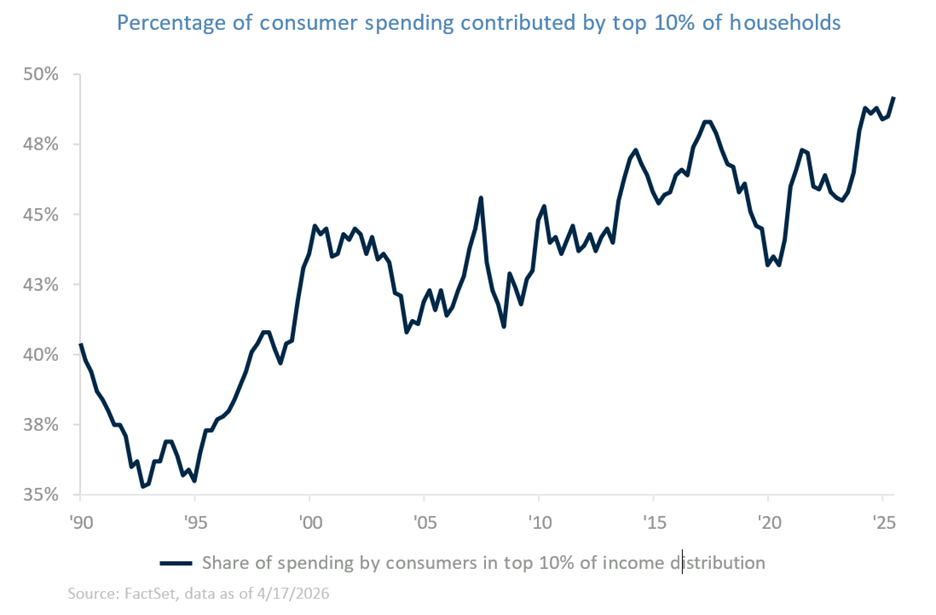

The growing divide between income groups is contributing to a more concentrated pattern of consumer spending, with a larger share driven by higher-income households. As a result, overall economic activity becomes increasingly dependent on a smaller segment of consumers, many of whom are more sensitive to changes in asset prices and financial market conditions. Currently, it is estimated that the top 10% of households generate nearly 50% of all spending, which translates to about one-third of US GDP. If this group pulls back spending due to equity market volatility or a significant market correction, the effects can ripple more broadly across the economy. This dynamic also has labor market implications, as lower-income households are often employed in sectors that depend on discretionary spending from higher-income consumers.

While some cyclical improvement is likely as inflation stabilizes and real incomes gradually recover, the structural forces underpinning a more K-shaped economy are expected to persist. Constraints around housing supply, elevated borrowing costs and unequal asset ownership continue to shape divergent household outcomes. Absent meaningful progress in affordability and broader participation in wealth-building assets, a full rebalancing appears unlikely. That said, these dynamics are not, in themselves, indicative of potential recession. Rather, they point to an expansion that is likely to remain uneven and increasingly reliant on higher-income consumers, with implications for the durability and stability of growth over time. While headline economic indicators remain resilient, the benefits of growth are not being felt evenly across households.

Bottom line

Elevated costs, higher borrowing rates and concentrated spending help explain the persistent weakness in consumer sentiment and suggest a more fragile and uneven expansion beneath the surface, though not one that is likely to result in a broad economic contraction or recession.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.

Raymond James financial advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Therefore, a response to a request for information may be delayed. Please note that not all of the investments and services mentioned are available in every state. Investors outside of the United States are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this site. Contact your local Raymond James office for information and availability.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Investment advisory services offered through Raymond James Financial Services Advisors, Inc.. TowneBank and Towne Wealth Management are not registered broker/dealers and are independent of Raymond James Financial Services. Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

© 2026 Securities offered through Raymond James Financial Services, Inc., member FINRA / SIPC

| Legal Disclosures | Privacy, Security & Account Protection | Terms of Use

Investment and Insurance products are:

- NOT A DEPOSIT

- NOT FDIC-INSURED

- NOT GUARANTEED BY TOWNEBANK

- NOT INSURED BY ANY STATE OR FEDERAL GOVERNMENT AGENCY

- SUBJECT TO RISK AND MAY LOSE VALUE