Differentiating between fundamentals and investor sentiment

Raymond James Senior Investment Strategist Pavel Molchanov explores why sentiment often diverges from fundamentals

The famed economist John Maynard Keynes said almost a century ago that “markets can remain irrational longer than you can remain solvent.” He was referring to the unpredictable nature of investor sentiment: an amorphous, hard-to-define concept that nonetheless plays a major role across various asset classes.

As investment strategists, our approach is grounded in fundamentals, such as interest rates and corporate earnings. But at the same time, it’s important to be aware that sentiment – that is to say, the market’s emotional state – also influences how investments perform, especially over relatively short timeframes. As vital as fundamental analysis is, an understanding of sentiment is also useful.

Meme stocks: Where sentiment supersedes fundamentals in the equity market

Fundamental analysis of stocks centers on earnings. The standard method of valuing a stock is a price-to-earnings (P/E) ratio. When the P/E multiple is high, a stock is typically referred to as “expensive” or “richly valued.” This does not mean that it’s necessarily a bad investment, but we typically want to see some justification for the lofty multiple, i.e., an expectation of high earnings growth in the future. For companies that have negative earnings, we can apply a revenue multiple instead. In certain sectors, other multiples are sometimes used, such as free cash flow yield in real estate and price-to-book value in financials.

But what if a company has no revenue? In other words, the firm is an early-stage business that has yet to begin selling a product or service. Traditional valuation analysis isn’t practical in these cases. It’s possible to create estimates for many years into the future, but these are prone to error. Share prices of such companies move from day to day based in large part on how the market perceives the company. Corporate announcements – R&D milestones, M&A activity, management changes – can influence sentiment, but even when there are no headlines whatsoever, sentiment is still subject to change.

You may have come across the term meme stocks. While there is no “official” list, the term refers to companies that, in general, 1) are on the smaller side; 2) have little to no earnings, and sometimes no revenue; and 3) are popular with day traders or momentum-oriented funds. Meme stocks are very sensitive to changes in sentiment, with share prices routinely swinging by double-digit percentages on a daily basis.

A single social media post can be enough to move meme stocks. While these stocks can be found in any industry, they tend to cluster around certain innovative or high-growth themes, such as quantum computing, nuclear technology, electric vehicles and cryptocurrencies (more on that last one later).

For our readers who may be tempted to invest in meme stocks, our message is: be careful. It’s certainly possible to ride a meme stock to hefty gains, but it’s also possible that any given meme stock will turn into a penny stock, or perhaps go out of business altogether. Precisely because they don’t lend themselves to fundamental analysis, meme stocks resemble lottery tickets. It’s a matter of luck rather than skill.

Precious metals: All that glitters can be volatile

Gold, silver and platinum all posted hefty gains over the past year, but – as with all commodities – they also exhibited intense volatility. Gold is the most sentiment-driven, while silver and platinum tend to be influenced more by “physical” supply/demand fundamentals.

Gold has a centuries-long history of being regarded as a one-of-a-kind metal, but why is that? The short answer is because that’s just how society looks at it. Gold’s special status in culture and the economy is ultimately a matter of sentiment rather than chemistry.

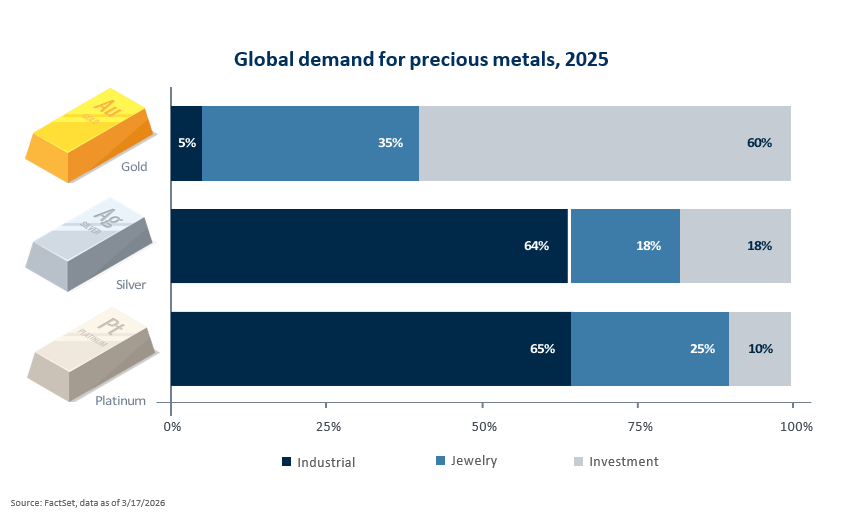

Industrial applications account for a mere 5% of global gold demand, whereas 60% represents gold as an investment (e.g., stockpiles in central bank vaults). The remaining portion is jewelry. The amount of gold mined around the world barely changes from year to year, so price volatility is largely a function of the level of investor appetite for owning gold. This appetite tends to increase in times of geopolitical turbulence and/or high inflation, but it is subject to abrupt reversals, sometimes for no apparent reason.

With silver and platinum, sentiment also plays a role, but physical demand is more important. Nearly two-thirds of global silver demand is attributable to industrial end markets, including 20% in solar panel manufacturing. In high-volume / low-margin products such as these, rapid escalation in input costs can create serious margin pressure. We are already seeing evidence of solar manufacturers starting to redesign their hardware to use copper in place of silver. Platinum is also vulnerable to commodity substitution, though to a lesser extent than silver. A key application for platinum is catalytic converters in auto engines, but because these are more highly engineered products than solar panels, redesign efforts are likely to take longer.

Cryptocurrencies: Sentiment on steroids

In thinking about which asset class is the most sentiment-driven, cryptocurrencies provide the prime case study. There is no fundamental underpinning to the value of Bitcoin, Ethereum, or other cryptocurrencies, with the exception of stablecoins.

Trading dynamics from day to day can be extremely volatile, even more so than meme stocks or precious metals. Among the reasons for this is the fact that cryptocurrencies are typically subject to less regulation than other asset classes. Cryptocurrencies have no governing authority, such as a central bank, and various trading platforms operate under a wide range of rules.

What makes stablecoins different from other cryptocurrencies is the emphasis on maintaining a stable value, typically $1.00/ unit. Stablecoins must be backed by assets, such as Treasury bills, that are low-risk and highly liquid. That said, stablecoins are not insured by the Federal Deposit Insurance Corporation, so they should not be looked at through the same lens as a bank account. If the company that issued any given stablecoin ends up going bankrupt, it’s possible to conceive a scenario where the stablecoin’s value could fall below par.

Entire mini-cultures have developed around some of the cryptocurrencies, with numerous blogs, podcasts and conferences. Celebrities and politicians occasionally endorse certain cryptocurrencies, which can result in gains that are rapid but also fleeting. Along the same lines, a critical news story can lead to sudden selling pressure. All of this means that cryptocurrency investors need to be ready for intense volatility, at any time. Given that sentiment plays such a central role, we are unable to provide price targets or even offer directional guidance for cryptocurrencies. Remember, they are ultimately just strings of digital code.

Bottom line

As much as we might wish for markets to always behave rationally, the reality is very different. Investors are human beings, who can be swayed by greed, fear, and every other emotion. While no asset class is entirely immune from sentiment-fueled volatility, some types of investments are more sentiment-driven than others. In the equity market, it’s meme stocks. In the commodity market, it’s precious metals, especially gold. Finally, cryptocurrencies across the board are particularly susceptible to abrupt shifts in sentiment.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

Raymond James financial advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Therefore, a response to a request for information may be delayed. Please note that not all of the investments and services mentioned are available in every state. Investors outside of the United States are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this site. Contact your local Raymond James office for information and availability.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Investment advisory services offered through Raymond James Financial Services Advisors, Inc.. TowneBank and Towne Wealth Management are not registered broker/dealers and are independent of Raymond James Financial Services. Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

© 2026 Securities offered through Raymond James Financial Services, Inc., member FINRA / SIPC

| Legal Disclosures | Privacy, Security & Account Protection | Terms of Use

Investment and Insurance products are:

- NOT A DEPOSIT

- NOT FDIC-INSURED

- NOT GUARANTEED BY TOWNEBANK

- NOT INSURED BY ANY STATE OR FEDERAL GOVERNMENT AGENCY

- SUBJECT TO RISK AND MAY LOSE VALUE