Navigating the economy, geopolitics and asset classes in the months ahead

Review the latest Weekly Headings by CIO Larry Adam.

- Despite the Iran conflict, US economic fundamentals remain on solid footing

- High-quality bonds remain part of balanced lineup

- Strong earnings and normalized valuations are supportive of the equity market

Over the past year, markets have been shaped by rapid advances in AI, elevated geopolitical tensions – especially involving Iran – and persistent uncertainty around global trade. In environments like this, successful investing rarely comes from chasing headlines or reacting emotionally. It’s about discipline, staying anchored to fundamentals and executing a clear long‑term game plan.

We frame our economic and market views on preparation, flexibility, and execution over short‑term noise. Here’s our playbook and targets for navigating the economy, geopolitics and asset classes in the months ahead.

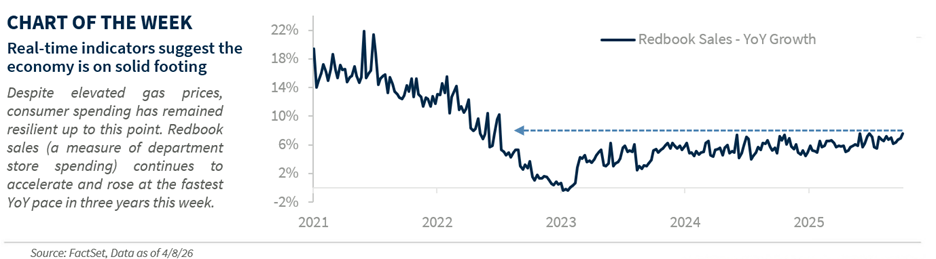

US economy remains insulated from energy spike

The recent surge in energy prices has raised concerns about the growth outlook, especially given that major oil spikes have often preceded recessions. That said, the US entered the Iran conflict from a position of strength. As a net oil exporter, with productivity gains helping contain inflation pressures and overall momentum still solid, our view is that the economy remains on firm footing. Real‑time activity indicators continue to signal underlying resilience, reinforcing our expectation that growth accelerates to 2.4% in 2026. The consumer remains an area to watch, as higher gasoline prices may weigh on sentiment, but tax cuts should help offset near‑term pressure. And if a durable ceasefire holds, energy prices should move lower, limiting the potential impact to discretionary spending.

The Fed faces a tactical dilemma

The Fed is navigating a particularly challenging environment, with inflation still running above its 2% target and a labor market increasingly making the case for eventual support. Adding to the complexity, higher oil prices are pushing inflation up in the near term while simultaneously increasing downside risks to growth. At the same time, Kevin Warsh is just a confirmation away from becoming the next chair. While Warsh’s experience makes him a credible choice, his long‑standing criticism of the Fed and appetite for reform suggest potential internal resistance, especially with Powell expected to remain on the Board of Governors after his term ends. History shows markets often test new Fed leadership, but with the inflation bump likely temporary, we continue to see room for one additional rate cut by year‑end.

Bonds remain a reliable anchor

High‑quality bonds often step up when portfolios need them most, providing steady income in calmer markets and cushioning volatility when risks rise. Despite the recent backup in yields, our base case remains that the 10‑year Treasury yield ends 2026 in the 4.25% to 4.50% range, supported by solid growth, a steady labor market and well‑anchored inflation expectations.

We expect yields to remain range‑bound, with a move below 4% unlikely without a recession and a break above 5% requiring either a growth shock or renewed inflation pressure. We continue to favor higher‑quality bonds – Treasuries, investment‑grade corporates, and municipals – over riskier sectors, especially with yields still above historical averages.

Fundamentals remain supportive of stocks

The recent equity market pullback is not surprising. We flagged several risks heading into the year, including elevated valuations, overly optimistic investor sentiment and midterm elections.

Importantly, the pullback has reset both valuations and sentiment, healthy adjustments that improve the market backdrop. With fundamentals still solid, we see reasons for optimism. We expect S&P 500 earnings to grow about 10% this year to $300, a conservative assumption versus the consensus near $319. Applying a 24x multiple – below last year’s closing level – supports our 2026 year‑end target of 7,250, or ~7% upside from current levels. We continue to favor US equities over other developed markets, as international equities face greater exposure to the energy shock, more hawkish inflation‑driven policy responses and fading currency tailwinds. That said, we continue to favor EM Asia.

Emphasize sectors with long-term secular tailwinds

This year has featured notable momentum shifts beneath the surface, especially as uncertainty remains elevated amid the Middle East conflict. In this environment, we continue to focus on sectors with long‑term secular tailwinds that can drive returns over time.

Technology, despite recent underperformance, remains a long‑term favorite, supported by strong revenue growth, upward earnings revisions and record margins. Industrials should benefit from rising defense spending and the ongoing AI buildout. We also favor health care, given attractive valuations, along with consumer discretionary, which stands to benefit from healthy household balance sheets and tax refunds. While energy has had a strong start amid the oil price surge, we expect oil prices to drift back toward $60 per barrel by year-end as the conflict eases, creating a headwind for the sector.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.

Raymond James financial advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Therefore, a response to a request for information may be delayed. Please note that not all of the investments and services mentioned are available in every state. Investors outside of the United States are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this site. Contact your local Raymond James office for information and availability.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Investment advisory services offered through Raymond James Financial Services Advisors, Inc.. TowneBank and Towne Wealth Management are not registered broker/dealers and are independent of Raymond James Financial Services. Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

© 2026 Securities offered through Raymond James Financial Services, Inc., member FINRA / SIPC

| Legal Disclosures | Privacy, Security & Account Protection | Terms of Use

Investment and Insurance products are:

- NOT A DEPOSIT

- NOT FDIC-INSURED

- NOT GUARANTEED BY TOWNEBANK

- NOT INSURED BY ANY STATE OR FEDERAL GOVERNMENT AGENCY

- SUBJECT TO RISK AND MAY LOSE VALUE