Inflation rears its ugly face, again

Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

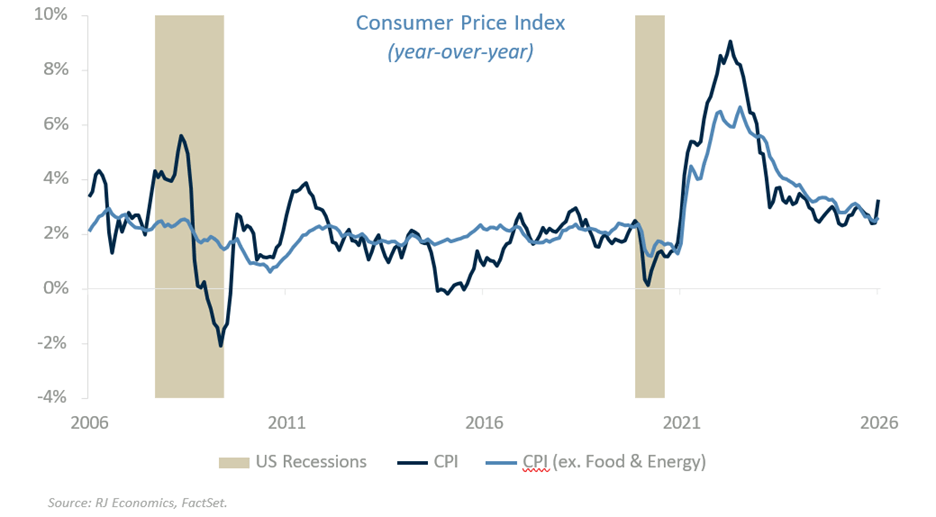

The question that is increasingly on everyone’s mind is simple: Is this time different? The answer will hinge squarely on what happens to core inflation, specifically the core Consumer Price Index and the core PCE price index. The Federal Reserve (Fed) is likely to remain patient if core prices stay contained even as headline inflation rises due to higher energy prices.

There are solid reasons to believe that this episode will differ meaningfully from what we experienced during the recovery from the pandemic recession. First, households today have far less excess savings than they did coming out of the pandemic, when accumulated cash buffers allowed consumers to absorb and accept price increases more readily. As a result, firms are likely to encounter much stronger resistance when attempting to pass higher input costs on to consumers.

In this context, the main inflationary risk does not stem from household excess savings but from the still expansionary fiscal environment created by the One Big Beautiful Bill Act, which has boosted tax refunds relative to recent years and provided sizable tax relief to businesses.

Second, labor market conditions remain weak and income growth has slowed accordingly. This was evident in February’s personal income report, which showed nominal personal income declining by 0.1%, matching the decline in nominal disposable personal income. More importantly, real disposable personal income fell by 0.5% on a month-on-month basis. In other words, purchasing power is eroding, making it increasingly difficult for consumers to sustain spending growth.

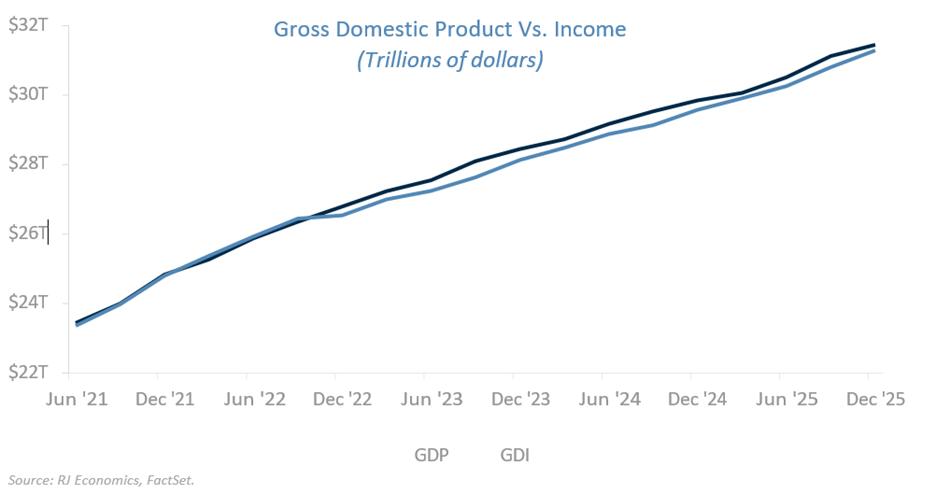

In February, household spending was supported by a further drawdown of savings, which pushed the personal saving rate down to 4.0% from 4.5% in January. This behavior may help smooth consumption temporarily, but it is clearly not sustainable. One important caveat is that income data are often revised and can be imprecise in real time. As recent data show, nominal gross domestic income has been systematically underestimated since 2022, suggesting that actual income growth may be somewhat stronger than currently reported. This implies that households may have slightly more financial cushioning than the official numbers suggest. Even so, this margin is unlikely to be sufficient for consumers to remain fully engaged in the economy without a renewed pickup in employment and income growth.

Bottom line

The latest CPI report was encouraging from the Fed’s perspective. For now, it reinforces our view that policymakers can look through the recent increase in headline inflation, as core prices remained well contained in March despite higher oil and gasoline prices. Headline inflation rose to 3.3% from 2.4% in February, but the underlying trend in core inflation remains favorable. As a result, we are maintaining our call for just one rate cut in the federal funds rate by the end of this year.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.

Raymond James financial advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Therefore, a response to a request for information may be delayed. Please note that not all of the investments and services mentioned are available in every state. Investors outside of the United States are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this site. Contact your local Raymond James office for information and availability.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Investment advisory services offered through Raymond James Financial Services Advisors, Inc.. TowneBank and Towne Wealth Management are not registered broker/dealers and are independent of Raymond James Financial Services. Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

© 2026 Securities offered through Raymond James Financial Services, Inc., member FINRA / SIPC

| Legal Disclosures | Privacy, Security & Account Protection | Terms of Use

Investment and Insurance products are:

- NOT A DEPOSIT

- NOT FDIC-INSURED

- NOT GUARANTEED BY TOWNEBANK

- NOT INSURED BY ANY STATE OR FEDERAL GOVERNMENT AGENCY

- SUBJECT TO RISK AND MAY LOSE VALUE